As companies with sustainability targets intensify efforts to reduce carbon emissions, the accuracy of Scope 3 GHG emissions reporting has become critical — especially in Categories 1 and 12, which cover purchased goods and end-of-life treatment. Current frameworks often overlook the climate benefits of biogenic carbon, creating inconsistencies that hinder progress toward meaningful decarbonisation.

This position paper, the result of a collaborative workshop on September 4, 2025, with the support of the Carbon Trust, proposes a shift to a more transparent and science-based approach to biogenic carbon accounting—one that aligns product and corporate reporting and empowers companies to fully recognise the impact of bio-based materials. If your organisation is serious about climate action, we invite you to read on and support this call for change.

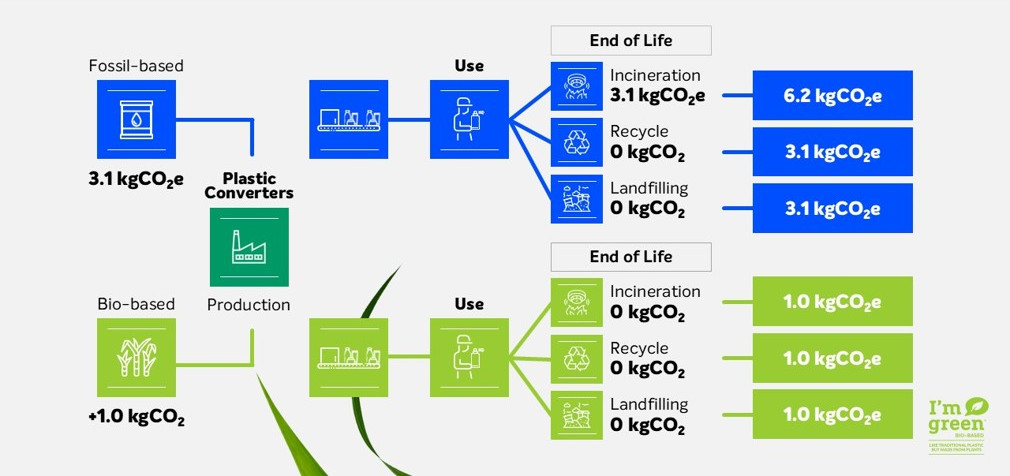

The following infographic uses I'm green™ bio-based polyethylene as an example, but the underlying reasoning is valid for any bio-based material.

This approach has consequences:

This approach solves all of the problems mentioned.

The negative carbon footprint -2.12 is an exemplification of I’m green bio-based HDPE and its LCA (life cycle assessment).

We, the undersigned, call for equivalent treatment of biogenic and fossil carbon in value chain GHG accounting and product carbon footprinting to support science-based decision making. We believe that this can only be achieved through GHG emission accounting approaches that recognise both uptake and emissions of biogenic carbon and the equivalent treatment of biogenic and fossil carbon on recycling and at end of life.

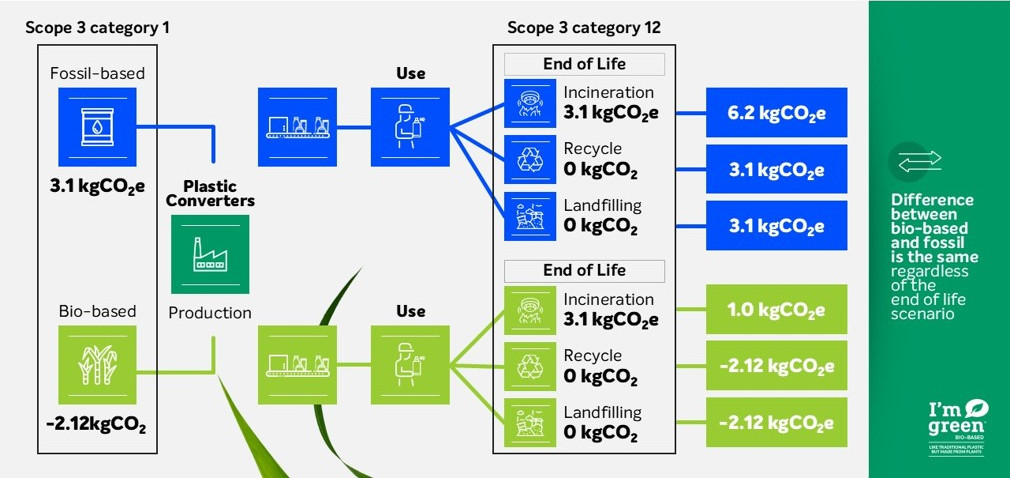

The purpose of this proposal is to address inconsistencies in how biogenic carbon is accounted for and to advocate for a consistent -1/+1 approach across emissions accounting frameworks. This approach aims to provide more realistic, accurate and transparent reporting of carbon flows.

This proposal is relevant to all biogenic materials, but its implications are especially significant in cases where a biogenic material serves as a substitute for a fossil-based incumbent material.

End-of-life (EoL) plays a pivotal role both in product carbon footprinting and corporate value chain accounting. Consistent carbon accounting across materials and end-of-life scenarios is essential to accurately reflect carbon flows and enable credible comparisons between fossil and biogenic materials. However, discussing the adequacy of such modelling considerations is outside the scope of this document (see appendices).

Recycling, incineration, landfill, or biodegradation differ in terms of greenhouse gas (GHG) emissions. The -1/+1 method, which is already used in LCA and CFP (Carbon Footprint of a Product), enables these differences to be transparently captured by tracing the release and retention of carbon over time, making the climate implications of circularity (e.g., recycling or reuse) visible and measurable in corporate GHG reporting. With increasing focus from corporations on reducing emissions at an organisational level, replacing fossil material with bio-based materials is an important strategy and therefore it is essential that the full benefits of biogenic materials are captured.

The biogenic carbon accounting rules for GHG Protocol’s Corporate Value Chain (Scope 3) standard and Product lifecycle accounting and reporting standard are not currently aligned, which presents a challenge when using product carbon footprints within value chain accounting. The difference relevant here is between the biogenic 0/0 approach which is implied within corporate accounting and the -1/+1 approach within product accounting. This difference is only applied to biogenic carbon, creating inconsistencies in accounting and making comparisons between bio-based materials and fossil materials impossible.

The following considerations are valid for all bio-based materials, but using bio-based plastics as example highlights the inconsistencies as they are molecularly identical to fossil plastics. They share the same physical properties regardless of the origin of their carbon content and will breakdown in the exact same manner. Despite this, whether a plastic’s carbon is of biogenic or fossil origin impacts end of life emissions accounting differently under current guidance.

For example, under the 0/0 accounting methodology used in corporate accounting for different end of life scenarios:

As shown in the examples above, the 0/0 approach for biogenic carbon has two main consequences:

When considering implementing a more circular economy, it is important to prioritise reduce, reuse and recycling before considering alternatives to virgin material.However, as circular systems are not 100% efficient – losses have to be replenished. Also, material consumption is expected to grow in the next decades due to increase in population and higher per capita consumption rates as affluence levels increase.

Organisations should be incentivised to adopt biomaterials to continue to drive emissions reductions. By being able to properly acknowledge the differences in carbon flows between fossil and biogenic materials, organisations would be able to utilise replacing fossil with biogenic material as a lever to help them achieve their reduction targets

Bio-based materials are not sufficient in themselves to promote a circular economy, but they play a pivotal role in advancing a truly circular carbon economy by drawing carbon from the atmosphere rather than tapping into geological fossil reserves. Sourcing carbon from renewable biobased sources and keeping it in a circular economy perpetuates net CO₂ reduction from the atmosphere. These shifts, supported by the carbon accounting methodology outlined in this letter, are necessary to capture the true carbon reduction potential of bio-based systems.

In summary, we recognise that biogenic accounting is a challenge shared across the industry, and propose that this is addressed by ensuring the -1/+1 approach is used across both organisational and product accounting and that there is consistent treatment of biogenic and fossil material at the end of life stage.

This document is focused on the embedded carbon, that is, the carbon which is contained in the product or material. When this embedded carbon is biogenic it is called the biogenic carbon content of the product or material, and it is the result of the balance between biogenic carbon uptakes and emissions during the several upstream life cycle stages. It can be calculated by the stoichiometry of the molecules or by elemental analysis and expressed in terms of CO2.

Mapping all the biogenic flows (uptakes and emissions) throughout the life cycle poses significant challenges, including but not limited to, the (inadequate) use of allocation factors between co-products to the carbon flows which can also lead to inconsistencies.

An important highlight is that the initial uptake (-1), when reported in category 1 of Scope 3 value chain accounting does not characterize a removal

[3]

. Category 1 is cradle-to-gate and therefore no permanence could be implied for a category that does not have use or EoL in its scope. Removals, if any, would appear as the balance between all scope 3 categories. When accurately reporting also downstream categories, especially categories 11 and 12 any removals would be visible as an imbalance between uptakes and emissions (see also modelling recycling and temporal boundaries and landfill).

Also of relevance are Land Use Change emissions which should be included both in product carbon footprints and also in corporate inventories. So if a product is made from biomass that caused a reduction in land-based carbon stocks, this fact should be included in the calculations. However, this does not affect the biogenic carbon content of said product which should still be represented by a negative number, but the loss of land-based carbon stock should also be added to the calculations.

The GHG protocol uses the cut-off approach to model recycling. In this approach the first life cycle (primary) is responsible for all upstream impacts while the second life cycle (secondary) is responsible for all activities necessary for recycling, but the recycled material itself enters the secondary free of burdens, with zero impact. From the perspective of the primary, the embedded carbon is fully transferred to the secondary and no emissions are assigned. As mentioned, this document does not discuss the adequacy or suitability of using this approach instead of others. However, the same approach has to be used for all materials regardless of their origin. If the fossil embedded carbon when recycled is considered as not emitted, the same assumption should be made for the biogenic embedded carbon.

Using again bio-based plastics as example, from the perspective of the primary, there is an initial uptake of CO2 during the cradle-to-gate stage, but there is no emission at EoL when it is recycled. For all practical purposes, there is a permanent removal. This is a consequence of the methodological approach used for recycling and not from the -1/+1 approach.

If this is cause for discomfort, we should question the methodological approach for recycling. If recycling is considered as a permanent solution for fossil carbon, since no emissions will ever be assigned to the primary, recycling bio-based carbon should be seen as a permanent removal. The use of the cut-off approach also means that all recycled materials are identical, regardless of the source of feedstock used in their manufacturing. Using plastics as an example, as the emissions from the recycling process are the same, recycled fossil plastic and recycled bio-based plastic have the same impact. It also means that if recycled bio-based plastic is subsequently incinerated at the EoL of the secondary product, there will be emissions of the embedded carbon just like a fossil plastic.

Some approaches have been suggested to solve this problem, such as assigning a virtual emission to the primary and another virtual uptake to the secondary in order to transfer the bio-based carbon content to the secondary. This apparently solves the problem, but from the perspective of primary, now recycling has the same impact of incineration, removing any incentives to circularity. If biogenic carbon is considered as emitted during recycling with another uptake in the secondary, the same consideration should be made to fossil carbon. Of course this also causes discomfort since now recycled fossil carbon would be equivalent to bio-based.

Ultimately this discussion is about who is responsible for the EoL emissions at final disposal. The cut-off approach assigns this burden entirely to the last life cycle to use the material. Further research and methodological development is needed to solve this problem. But the problem is the same both for bio-based and fossil materials and whatever approach is chosen should be consistently applied to all materials. It is unfair to single out bio-based materials only as it is done today.

There is currently research being done on modelling approaches that consider multiloop cascading recycling that could inform future developments also in this field.

Time appears in GHG accounting in two different ways. The first is what emissions (today and/or future) should be considered in our carbon footprint or corporate inventory. This is the time horizon at the inventory level. Another way is the time horizon for impact assessment, that is, for how long should we consider the impacts after an emission happens and that is the time horizon for the impact assessment. This latter has been solved when we adopted GWP100 as the metric, although the implications of this choice have never been deeply discussed.

There is much less clarity on the time horizon at inventory level. When we consider that there is no time horizon (or an infinite time horizon), all future emissions should be accounted for as if they had happened when the product was put on the market. This means that all emissions, present and future, are equally important which is justified by the inter-generational equity principle of the sustainable development definition. On the other hand, when we establish a time horizon after which no emissions are considered we are placing greater value on present emissions over those of the future.

A 100-year time span allows us to focus on the impact of the climate crisis now giving greater weight to more potent gases such as methane, whilst using an infinite time horizon may obscure this rate of change occurring at present. Conversely short-term time horizons may not capture cumulative warming events.

This discussion is very pertinent for modelling landfills, which are still the cheapest and most used EoL treatment worldwide. The datasets available in the major databases all contain an implicit time horizon of 100 years as that is the limit for accounting for emissions from the landfill. For plastics, the rate of degradation is assumed to be less than 1% and even for materials that are considered biodegradable, only a fraction is degraded in 100 years.

But the solution may not be as simple as developing datasets with an infinite time horizon for landfills. Materials such as glass and metals have emissions concentrated in the manufacturing stage and virtually no emissions at EoL. On the other hand, materials with carbon have significant emissions at EoL which, when landfilled, may happen in decades or centuries from now. When all future emissions are grouped now, we obscure this fact and we might make choices that exacerbate the rate of change now.

Both 100 year and infinite views are necessary for a complete picture of the climate change impacts.

It is standard practice to consider that food, feed and fuels are very short lived products and modelling the biogenic carbon flows using the -1/+1 approach would not be justified and an exception should be granted for them. And this is usually true today, but as alternatives to recycle waste into fuels and products become more common, modelling the carbon flows also for these types of products may become important.

[1]

The GHG Protocol uses an infinite time horizon, therefore no explicit mention to 100 years is made. However, datasets (such as Ecoinvent, Sphera, etc) used to calculate landfill emissions use a 100-year cap for emissions.

[2]

The emission of the embedded carbon is roughly the same size as the cradle-to-gate PCF of fossil plastics. This difference is therefore around 50% or more.

[3]

IPCC defines Carbon Dioxide Removal as “anthropogenic activities that remove CO2 from the atmosphere and store it durably in geological, terrestrial, or ocean reservoirs, or in products”. Therefore there is a requirement for permanence.

Changing Scope 3 accounting rules for biogenic carbon is essential to fully capture the contribution of bio-based materials to climate change mitigation.

We invite you to add your voice to ours.

Signing this petition does not imply endorsement of the I’m green™ bio-based brand or its products. This petition solely reflects the support for the broader principles or actions outlined in the above statement, wholly independent of commercial affiliations.

This letter has been facilitated by the Carbon Trust